Kerrisdale Capital - Sahm Adrangi

$1.11B AUM, 54 Holdings

Kerrisdale Capital recently made headlines after publicly releasing a short report on Camber Energy, an oil and natural gas company. Sahm Adrangi is no stranger to being transparent on social media; he joined Twitter in 2012 and before that, he was posting anonymously on SeekingAlpha under the moniker “ChineseCompanyAnalyst.” Adrangi was eventually outed by a Bloomberg reporter as the man behind the account.

After graduating from Yale University with a BA in Economics in 2003, Adrangi started his career at Deutsche Bank. With roughly two years of investment banking experience under his belt, Adrangi left to join Chanin Capital Partners, and then Longacre Fund Management. In 2009, Adrangi finally decided to head out on his own and founded Kerrisdale Capital. Adrangi started trading with $300,000 of his and his family’s money in an apartment in East Village, New York. He eventually convinced a hedge fund recruiting firm to rent him an empty desk in their office. The rest is history.

Adrangi gained notoriety in 2010 after making several successful short calls on Chinese companies that he noticed had accounting irregularities and shady auditing practices. He observed that China Education Alliance was claiming vast amounts of revenue and growth with high margins, even though their website looked like it had been created by a fifth-grader who had just completed a beginner’s course on coding, among other irregularities. Adrangi hired a private investigator to examine the company’s training center in China, which was found to be almost empty. Confident that the company was misrepresenting its financial metrics, Adrangi shorted China Education Alliance with 20% of his entire portfolio. Adrangi wasn’t alone; he made his short announcement and research publicly available on SeekingAlpha. The stock subsequently dropped 40% the next two days, and Kerrisdale finished up 60% that year.

“In terms of how we’ve separated the frauds from legitimate companies, we’ve relied on investigators, financial filings in China, and common sense. Some of these businesses are reporting irrationally high margins, growth rates and returns on capital despite operating commodity businesses. These too-good-to-be-true situations have led us to dig deeper on whether these companies are misrepresenting themselves in their filings.”

-Sahm Adrangi

In 2011, Adrangi returned 180%. By the end of 2012, Kerrisdale was regarded as one of the best-performing hedge funds in America based on 3 year returns by the Barclays Hedge Fund Index.

“In this business, you can be a total weirdo, be a nice guy, whatever. All that matters is where your returns are.”

-SA

Last week, I published a pay-walled newsletter detailing the top-performing funds based on 3 year returns. The list includes 2 veteran fund managers who are rarely mentioned in the media and 1 relatively younger fund manager. Check it out here:

Camber Energy Short

On October 5th, Kerrisdale announced on Twitter that they were short shares of Camber Energy (CEI). That day, shares of CEI opened at $3.01 and closed at $1.53, down 49%. CEI trades at $1.35 at the time of writing. Kerrisdale highlighted several key points on why they are short:

CEI has failed to file financial statements to the SEC since Sep. 2020.

Only asset is a 73% stake in Viking Energy.

Viking’s shareholder equity/book value is -$15 million.

Camber’s partnership with ESG Clean Energy raises concerns, as ESG Clean Energy is owned by the Scuderi Clan, which has faced SEC sanctions in the past.

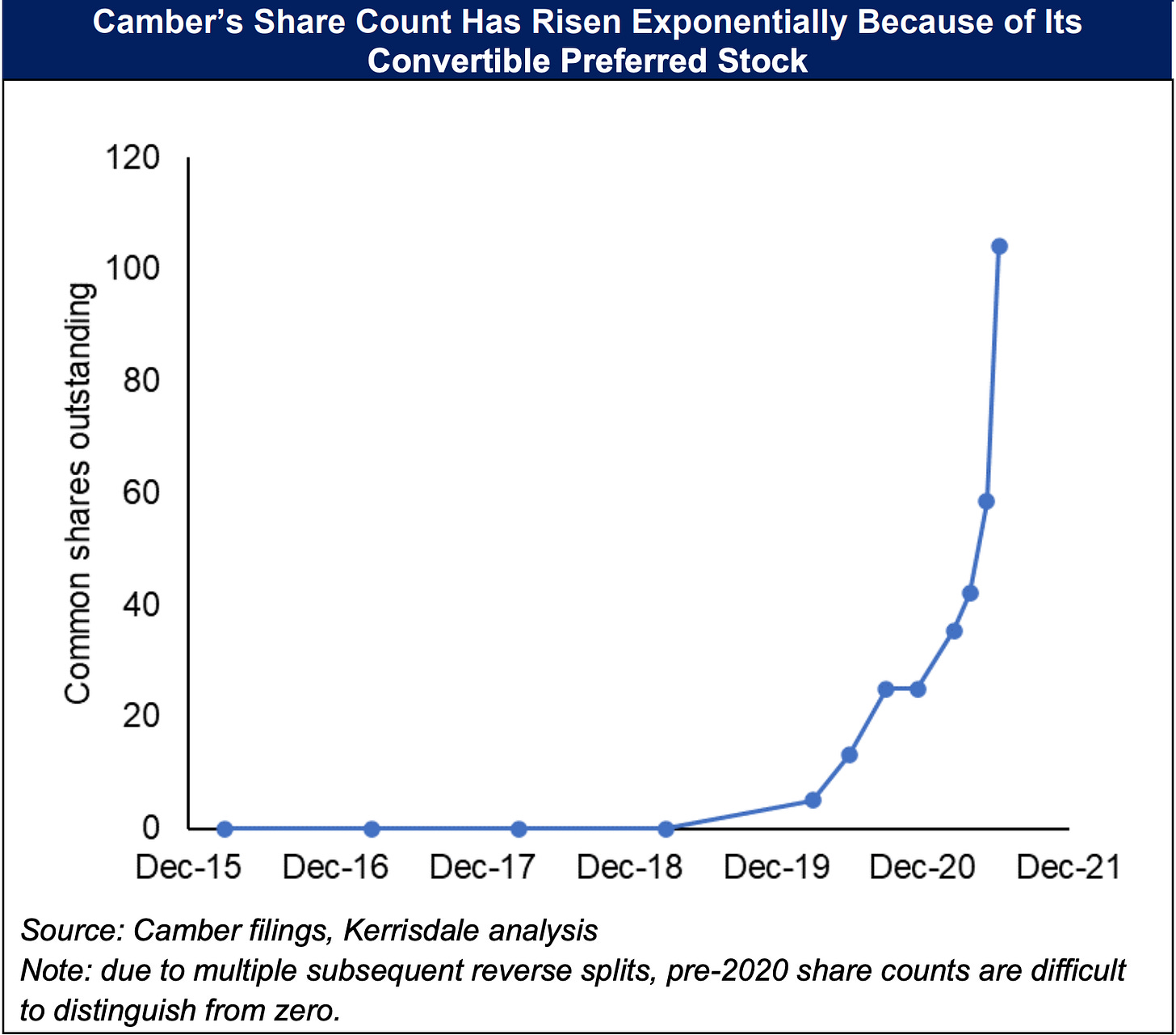

Kerrisdale believes Camber’s fully diluted share count is triple what the company reports.

Share count has increased 50 million-fold from 2016 to July 2021.

“We estimate that, of the 104.2 million common shares outstanding on July 9th, 99.7% were created via the conversion of Series C preferred in the past few years – and there’s more where that came from.”

“Is there any logic to this bizarre frenzy? Camber pumpers have seized upon the notion that the company is now a play on carbon capture and clean energy, citing a license agreement recently entered into by Viking. But the “ESG Clean Energy” technology license is a joke.

Not only is it tiny relative to Camber’s market cap (costing only $5 million and granting exclusivity only in Canada), but it has embroiled Camber in the long-running escapades of a western Massachusetts family that once claimed to have created a revolutionary new combustion engine, only to wind up being penalized by the SEC for raising $80 million in unregistered securities offerings, often to unaccredited investors, and spending much of it on themselves.”

-Kerrisdale Capital Short Report

Performance & Holdings Value

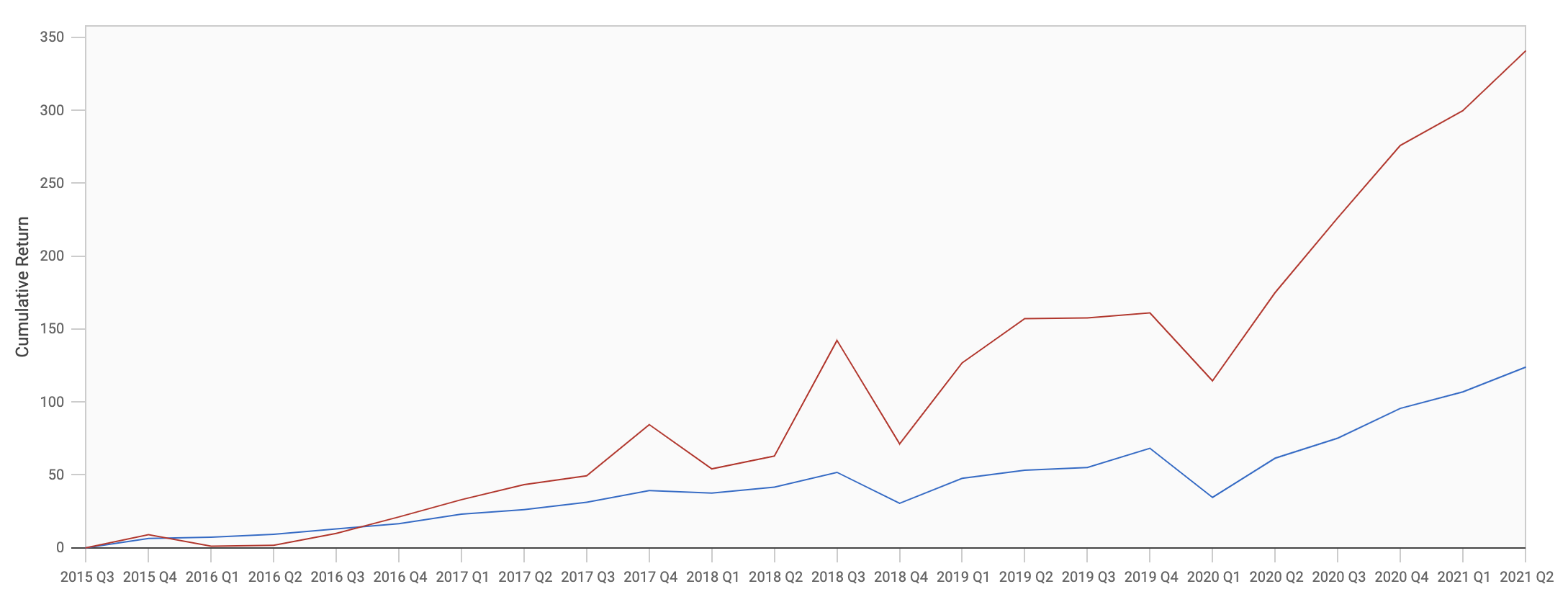

Red Line: Kerrisdale Cumulative Return (324%)

Blue Line: S&P 500 Cumulative Return (124%)

Since Q3 of 2015, Kerrisdale has returned an estimated 341%, more than doubling the S&P 500’s return of 124% in the same period. The fund currently has a 37.38% portfolio allocation in information technology stocks and a 31.54% allocation in communications stocks.

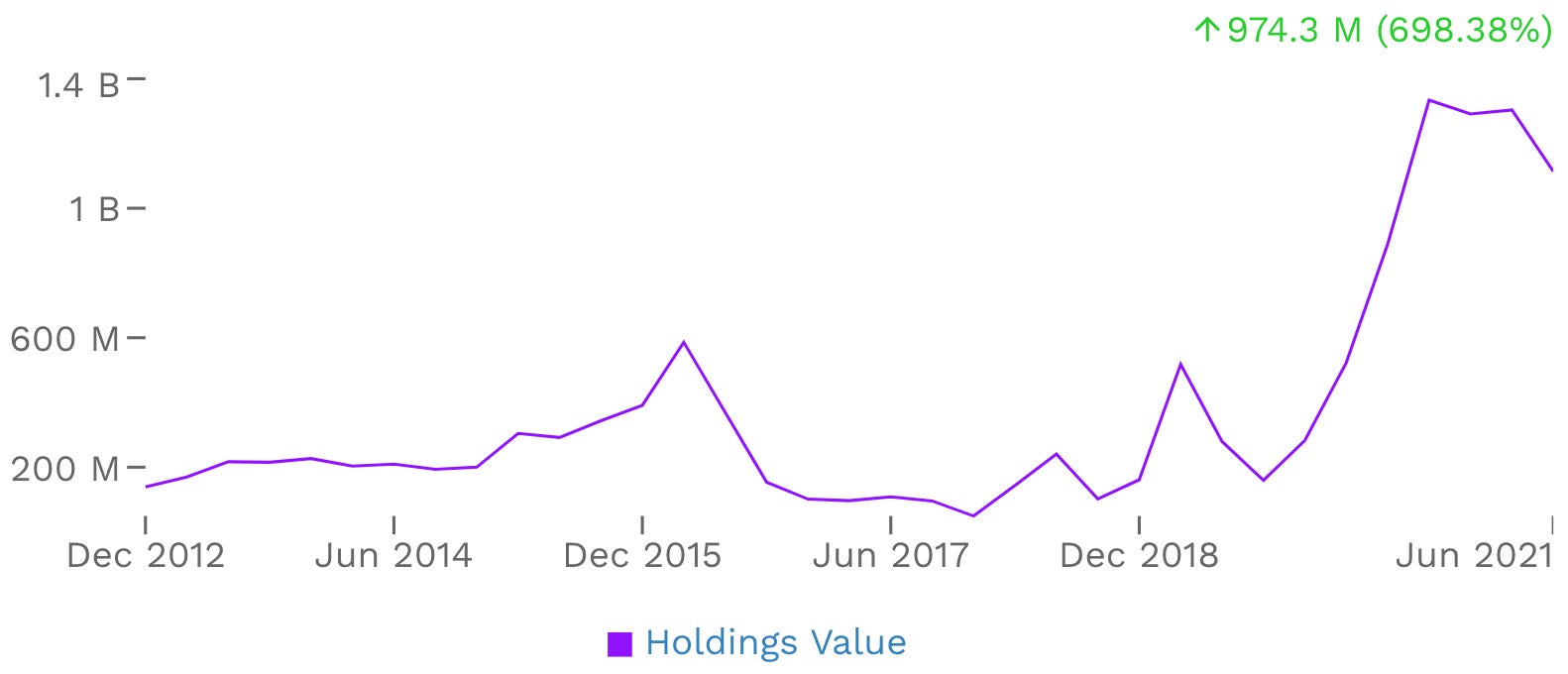

Kerrisdale’s holdings value sits at $1.11 billion, down 14.57% from Q1. This is due to Adrangi taking gains, and not losing money, as Kerrisdale returned an estimated 10.22% during Q1. It will be interesting to see whether the fund’s holdings value increases or decreases due to new buys/sells during Q3. My prediction is that it will increase.

Current Portfolio

Kerrisdale has a top 10 holdings concentration of 42.51% and a top 15 holdings concentration of 57.84%. Kerrisdale can be considered an active fund, as the average time a company is held in their portfolio is 3.17 quarters. The average time a company is held in their top 10 positions is 1.3 quarters, while the average time held for a top 20 position is 2.3 quarters.

The fund’s top position, INFO, may be the least known ticker among their top 5 positions. INFO operates as a software information and analytics provider to customers in the business and government world. S&P Global announced plans to acquire INFO for $44 billion last November, and it was recently announced that the deal was set to secure EU antitrust approval. INFO is up a healthy 35.4% YTD, compared to the S&P 500’s 20.7% return.

Significant Changes

Kerrisdale increased their TWTR position after reducing their exposure during Q1. The fund increased their CRM position by 67% during Q2; this was a timely buy as shares of CRM increased 10.7% during Q3.

Kerrisdale reduced their exposure to Asia during Q2, cutting shares of SE, TIGR, and JD. Selling TIGR was a great move in hindsight, as shares plummeted 59% during Q3. Selling SE, not so much; shares rose 17% during Q3 and are up 80.7% YTD.

Kerrisdale has remained a transparent fund since their inception, oftentimes publicizing their positions and research on social media. In 2013, Kerrisdale had 1,925 Twitter followers. Today, they have over 68,000. Driven by Adrangi’s tenacious and unfiltered personality, Kerrisdale remains a valuable fund to learn from.

Follow Kerrisdale on Twitter @KerrisdaleCap

Hedge Vision - Institutional Insights

Please don’t hesitate to send me topic recommendations, suggestions, or general questions. You can contact me by email: HedgeVisions@gmail.com, or by Twitter messages @HedgeVision

Disclosure: Of the equities mentioned above, I own BABA, FB, CRM, FB, JD, SE, & AMZN via common shares.

Source 1 - Sahm Adrangi LinkedIn