July 2024 Portfolio Review

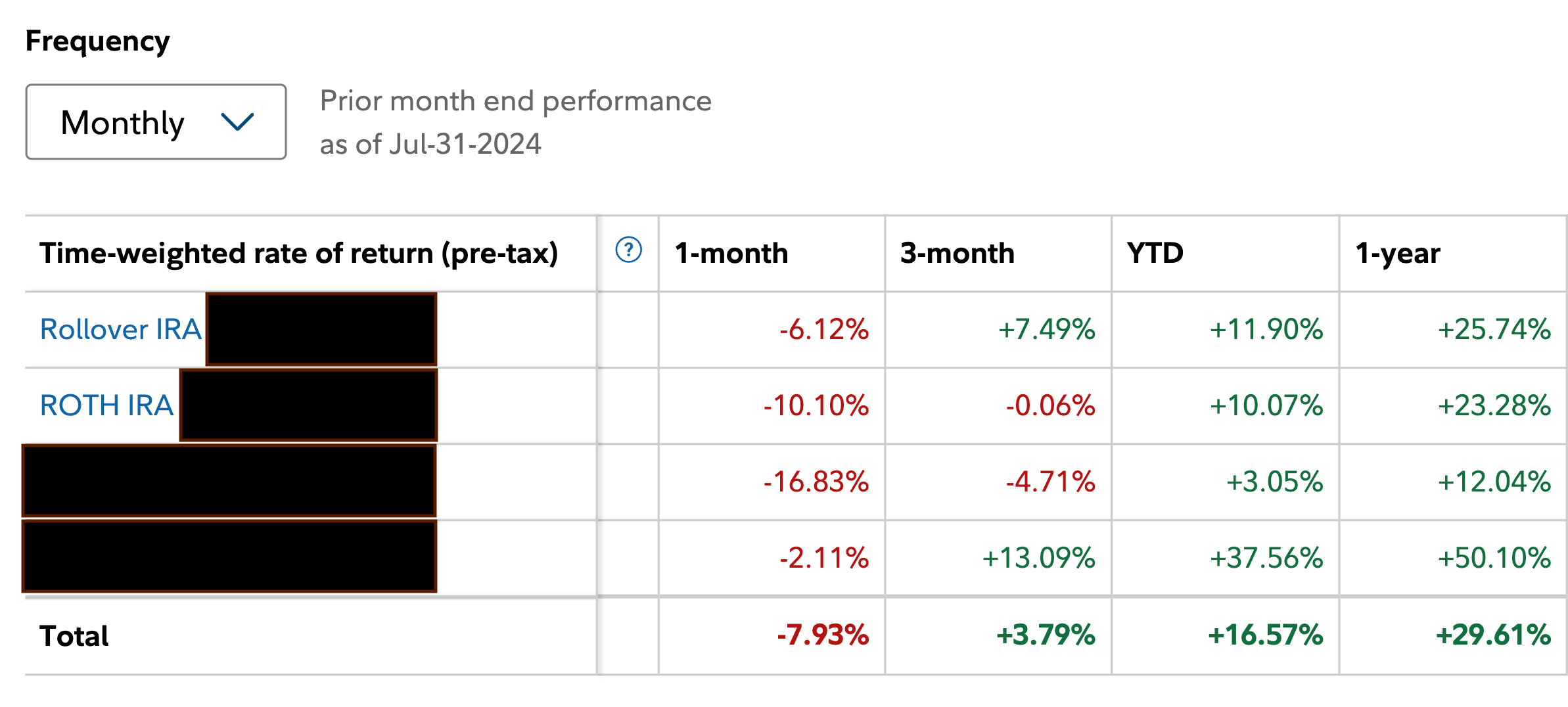

The Hedge Vision portfolio has returned 16.57% YTD

July proved to be a wild card for the market, with the S&P 500 returning 0.94% and the Nasdaq 100 losing 2.24%. The Nasdaq 100 was extremely close to entering a technical correction, declining by 9.78% from peak to trough between July 10 and July 30.

During July, the Hedge Vision portfolio declined by 7.93%, bringing its YTD return down to 16.57%. That compares to the S&P 500 and the Nasdaq 100’s YTD returns of 17.36% and 17.56%, respectively. My portfolio is still outpacing both of the indices on an annual basis.

By percentage, PYPL was my top July gainer with a 13.79% return followed by DHR at 13.32%.

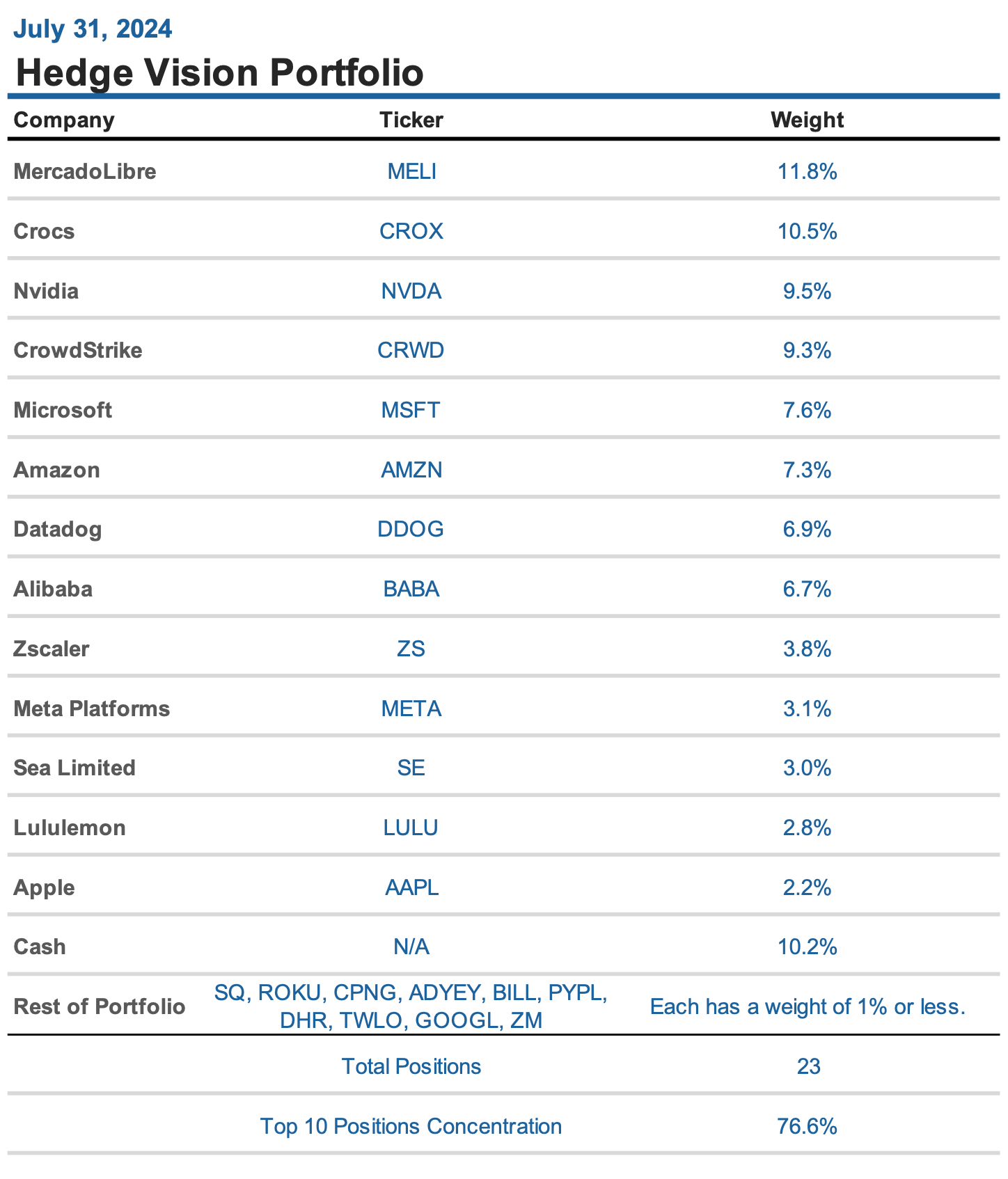

Total Positions: 23 compared to 26 as of Dec. 31

Top 10 Position Concentration: 76.6% compared to 73.8% as of Dec. 31

Rest of Portfolio: 13.2% compared to 19.4% as of Dec. 31

Cash: 10.2% compared to 6.8% as of Dec. 31

My losses were led by my largest position, Crowdstrike, which fell by 40.85% following an outage that affected 8.5 million Microsoft Windows devices. CRWD was my largest position at the beginning of the month with a 14% allocation.

I own CRWD in 3 accounts with a cost basis of $95.09, $95.10, and $156.64. I didn’t make any changes to my position during July.

My Thoughts on the CrowdStrike Outage

My long-term conviction in the company remains unchanged following the outage. However, CRWD will likely remain muted in the short-term as there is now an element of uncertainty surrounding the company.

The outage was NOT the result of a breach or hack but rather because of a faulty sensor configuration update. It says nothing about the safety or efficiency of CrowdStrike’s actual cybersecurity products.

With that in mind, the outage will still have an effect on the company’s future sales and margins for a few reasons:

CrowdStrike said it would provide credits to its affected customers.

In addition, the company’s reputation has been damaged, which could result in delayed or lost deals.

To top if off, CrowdStrike could be the recipient of lawsuits and regulatory fines. Insurer Parametrix estimates that Fortune 500 companies, excluding Microsoft, lost $5.4 billion as a result of the outage.

The following is CrowdStrike’s limitation of liability policy in its purchase order terms, which should provide the company with some legal protection:

CrowdStrike hasn’t yet announced the date for its next earnings, which may prove to be the company’s most important earnings yet.

The situation is extremely unfortunate although I’m confident that CrowdStrike will be available to recover due to its best-in-class cybersecurity products and high level of government clearance.

CRWD is one of my oldest holdings and I’d be interested in buying more if the price declines to the $200 range.

July 2024 Buys

New Positions: Lululemon (LULU)

I started a new position in Lululemon at the beginning of the month using a dollar-cost average strategy and made six separate purchases in July.

At the beginning of the year, I had Nike (NKE) on my watchlist. However, after watching LULU fall by 40% YTD, I couldn’t get myself to start a position in Nike.

At current prices, LULU is a much better deal than NKE and has a solid lead in revenue CAGR, gross profit margins, and free cash flow per share. Yet, the market still rewards NKE with a much higher forward P/E multiple.

Why? It’s because Nike is one of the most recognized brands in the world, if not the most. However, its status as the sportswear leader has come under fire in recent years in light of new contenders, which include Lululemon, Alo, Hoka, and On.

Nike can absorb a few quarters of underperformance, but if the trend persists, its premium multiple will at risk.

Meanwhile, LULU is trading at its lowest forward P/E since 2009 and has shed 53% YTD. The company is still the leader of athleisure, a trend I expect to remain relevant for years to come.

A resumption to 20%+ revenue growth seems possible given exceptional international growth (45% in China, 27% in rest of world) and men’s market share expansion in the U.S.

You can read more about my Lululemon thesis here:

Increased Positions: None

All of my buys and sales in real-time, along with further analysis and commentary, are shared with contributing members on Substack Chat:

July 2024 Sales

Exited Positions: None

Reduced Positions: None

Plan for August

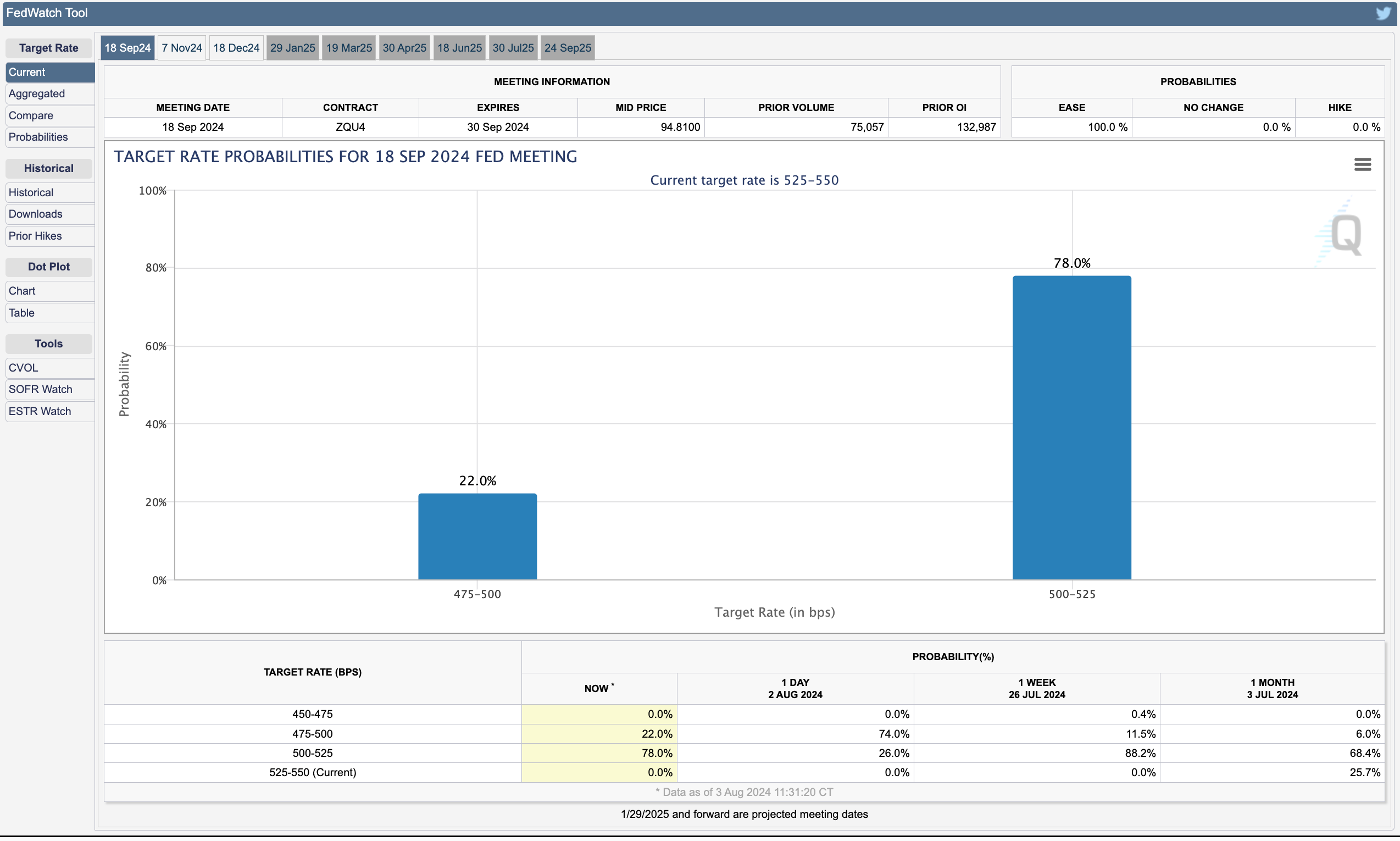

The market seems primed to go higher with a rate hike on the way and inflation falling lower. CME’s FedWatch tool currently shows that the market is pricing in a 100% chance for a rate cut in September. However, it’s still important to avoid complacency.

(I wrote the above paragraph near the end of July when sentiment was still fairly bullish. The beginning of August has tempered expectations significantly.)

AMD may have bailed out Nvidia and the market as a whole with its positive earnings report. A poor report could have sent NVDA even lower, taking down the Nasdaq 100 to a technical correction zone and likely lower. NVDA was down by 16.55% MTD as of July 30 before surging higher by 12.81% on the last day of the month with another post-close gain of 3.67%.

Fortunately, AMD’s earnings pointed to increased demand for AI services, with its data center revenue growing by 115% YoY to $2.8 billion. Unfortunately, all of AMD and NVDA’s gains have been erased since then.

My only new position compared to the beginning of the year is LULU as great deals have largely been taken off the shelves given the market’s generous returns. I’ve also added to three of my existing stakes: MELI, ZS, and BABA.

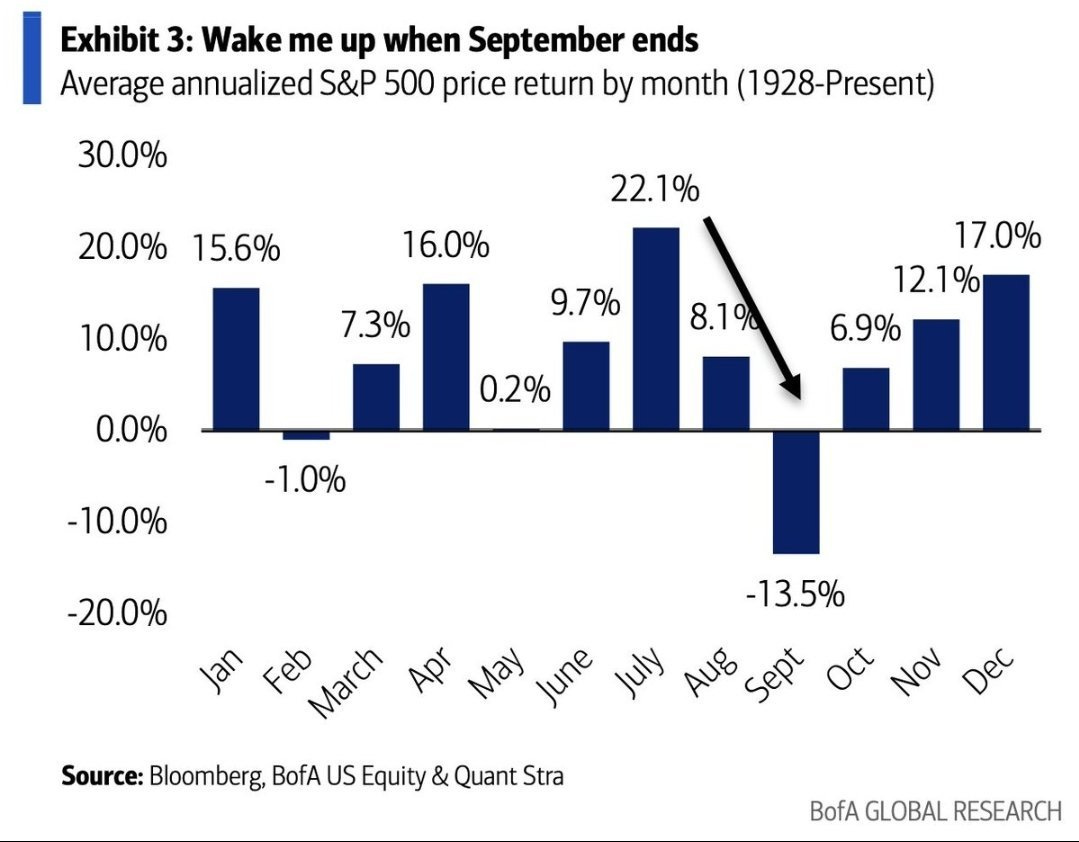

I look forward to the opportunities that could present themselves as we enter what has historically been the most challenging three month stretch of the year.

Hedge Vision - Institutional Insights

Thanks for reading!

📖 Join the conversation on Substack Chat

🕊️ Get real-time insights on X/Twitter: @HedgeVision

📧 Old school is cool too: HedgeVisions@gmail.com

Thoughtful analysis of Nike vs Lulu in terms of brand and competitive positioning. Agree that Lulu stock is cheap here and Nike probably has some more work to do to get through their issues.