Fintech Flop: When Disruption Leads to Destruction

Most fintech stocks have left investors disappointed

The promise was to revolutionize finance with a new portfolio of digital tools available in the palm of your hand. Unfortunately, most fintech companies haven’t lived up to their expectations.

SOFI, UPST, COIN, and HOOD. What do these four fintech companies have in common?

They all had their IPOs after 2020, which is true of many of the fintech stocks popular among retail investors. They’ve also underperformed the market by a wide margin:

Finding a post-2020 fintech IPO that has outperformed the market is quite a challenge. FOUR was the only company that I was able to find.

18 of the 19 companies failed to outperform the market, or a failure rate of 94.7%. This isn’t a result of cherry-picking data, as I have included the majority of fintech IPOs since 2020.

Even worse, only 4 companies on the chart provided positive returns: FOUR, NU, BILL, and UPST.

Could the poor returns be attributed to rising rates? When comparing these stocks with the federal funds rate, an inverse relationship is visible.

With higher rates, all stocks carry a lower valuation based on the discounted cash flow (DCF) model. Fintech stocks are hit even harder due to increased borrowing costs for companies and customers, reduced lending profitability, and a higher risk of loan defaults.

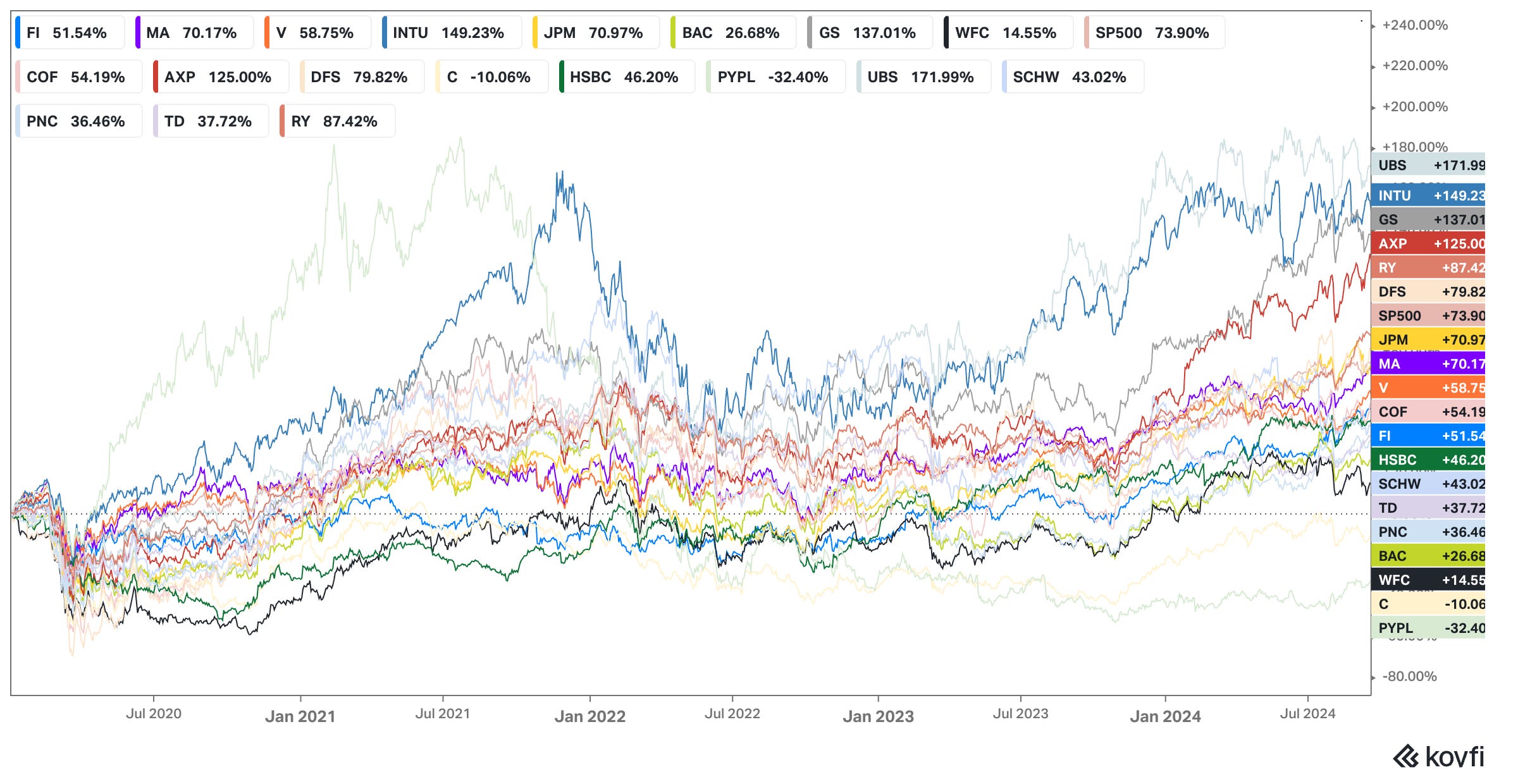

That theme is less prevalent when you look at the returns of legacy financial firms, or the companies that the so-called disruptors are trying to disrupt:

These companies have enjoyed much higher returns than their flashy competitors. 6 of the 19 companies have outperformed the market since 2020.

To be clear, I’m not advocating for an investment in these financial incumbents. However, the data clearly shows that the average legacy financial stock has generated better returns than the average fintech stock since 2020.

Why Fintech has Failed to Flourish

Fintech companies set out to modernize the financial industry and challenge existing incumbents by providing digital solutions for their customers.

At the same time, none of the solutions that they provide are unique. They can digitalize the loan process and incorporate AI into lending, but so can any other financial institution with deep enough pockets.

In other words, finding a moat in fintech is extremely difficult.

A prime example of this is SoFi. The company offers a variety of services, which includes lending, investing, banking and credit cards. However, none of these services are unique. If anything, SoFi’s competitive advantage lies in its simplicity, not in its services.

Meanwhile, emerging fintech companies have a natural disadvantage when it comes to their larger competitors due to elevated marketing costs and a lack of economies of scale.

For example, larger banks can typically provide more favorable loan and deposit rates due to their size and risk-profile, which can bring along regulatory advantages as well. Emerging companies can also offer competitive rates, although this is enacted as a loss leader strategy in many cases.

This doesn’t mean that large financial firms are invincible. It just means that the odds are stacked against their smaller competitors in a crowded market.

Falling Rates Could Benefit Fintech Stocks Again

Earlier this month, the Fed announced a 50 bps rate cut to between 4.75% and 5.00%. This was the first rate change since July 2023.

Flash forward a few months to Nov. 2023, which is when many of the post-2020 fintech IPOs began to heat up as the market started to price in rate cuts. Year-over-year, 12 of the 19 companies have outperformed the S&P 500:

Falling rates can lead to higher demand for several financial instruments, such as loans and mortgages. At the same time, it also echoes the Fed’s message of a weakening economy.

An argument that could be made is that many of the stocks in the fintech IPO boom of 2020-2022 carried too high of a valuation during their debut given the low interest rate environment. Now, these stocks are growing into their valuations with rates set to fall during the next few years.

A comeback in fintech stocks has certainly materialized, although those who invested two years or more ago are likely still down on their investment.

Final Thoughts

Based on a scarcity of sustainable competitive advantages and a high sensitivity to macroeconomic conditions, investing in the fintech space is an extremely tricky and difficult process.

At the end of the day, the competitive advantages in fintech companies seem to lie in their consumer acceptance and brand awareness rather than their services. Whether these are real competitive advantages that will be able to provide market-beating returns over the long-term remains the big question. It hasn’t gone well so far.

Hedge Vision - Institutional Insights

Thanks for reading!

📖 Join the conversation on Substack Chat

🕊️ Get real-time insights on X/Twitter: @HedgeVision

📧 Old school is cool too: HedgeVisions@gmail.com