Awareness of Investing Fallacies

Awareness of Investing Fallacies

5 Logical Fallacies

A fallacy is defined as “a mistaken belief, especially one based on unsound argument.” Investing is just as much a psychological game as it is a research-based profession. Even the most experienced investors can fall prey to fallacies.

Price-Anchoring Fallacy

Example: Jenny purchased shares of Cloudflare for $30. After a few months, Cloudflare had risen 33% to $40, so Jenny was satisfied with her gains and sold out. However, in the next few months Cloudflare skyrocketed to $80. Meanwhile, Jenny never bought back because she had sold her Cloudflare shares at a much lower price and did not think that buying higher would be a good idea.

This is probably the investing fallacy I struggle most with. Buying a stock back at a higher price after you sold at a lower price hurts the ego and confirms that you made a mistake that you regret. An experienced investor should be willing to buy back a stock at a higher price and admit that they were wrong as long as their original investment thesis for the underlying company remains intact.

Price-anchoring is also seen in everyday activities. When you shop online and see an item on sale compared with the original price, chances are that the item was never really the original price. With a side-by-side comparison, the sale price will look like a much better deal.

Price-Anchoring Example Recency Bias

Example: Jenny has been waiting for Apple to drop lower to her price target and today, it finally does. However, now she is unsure about purchasing shares and the large price decline is making her nervous. “It’s fallen so much and it will probably fall more, so I should wait to buy cheaper” is what Jenny thinks at the moment.

Recency Bias Example This may be one of the most common investing fallacies to plague investors. Large price declines in individual companies as a result of macroeconomic events and not as a result of any company specific news are oftentimes perceived as a fundamental decline in the individual company. A stock’s price is not 100% indicative of a company’s financial well-being in the short-term.

2 examples of top-performing hedge funds that started shortly after the Dotcom Bubble include Tiger Global and Altimeter Capital.

“You take somebody like Tiger Global and Chase who started in 2000 right after the dot-com blowup. So there was plenty of examples in my world of folks who started small during periods of duress driven by deep conviction and their own capabilities. And so, for me, it seemed from the outside looking in like I was crazy, but it made perfect sense to me.”

-Brad Gerstner, CEO & Founder of Altimeter Capital

Sunk Cost Fallacy

Example: Jenny invests $1,000 in Enron. Just a few months later, Enron drops in value by 50%, leaving Jenny in a tough situation with a difficult decision to make. Jenny decides to hold because she doesn’t want to lose money on her initial investment, even though she has read several reports questioning the validity of Enron’s business model. She rationalizes that she might as well hold until her investment breaks even, then sell out immediately.

Sunk Cost Example From August 2000 to December 2001, Enron’s stock price plummeted from $90 to $0.26. Looking back, Jenny would have been much better off if she had decided to take the 50% loss instead of the 99.7% loss.

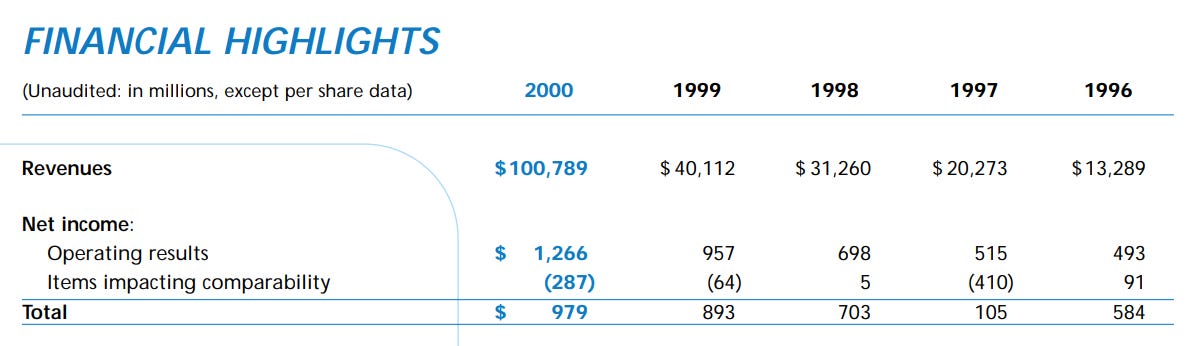

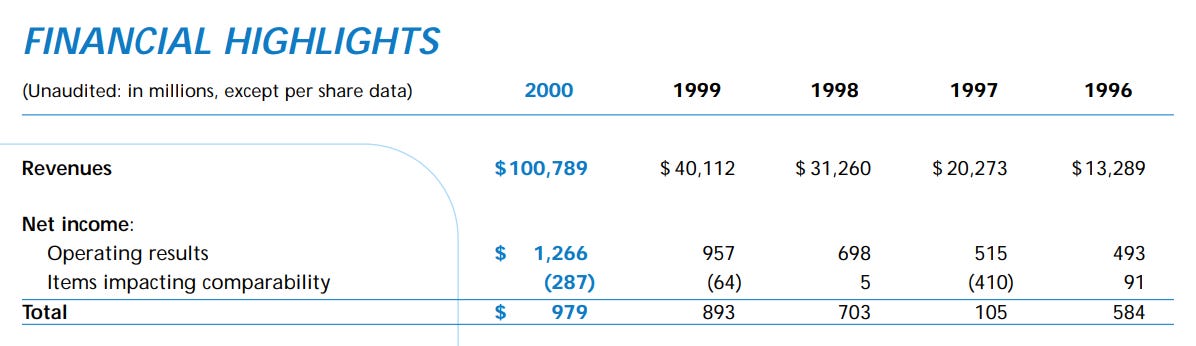

The sunk cost fallacy can be mostly avoided by performing proper due diligence before buying a stock and while owning the stock. Enron was originally an energy company before moving on to trading a variety of volatile derivatives that ultimately led to their bankruptcy. The very basis of the company itself sounds extremely risky, although investors were drawn in by fraudulent earnings. It’s worth admitting that I am luckily speaking from hindsight bias; Enron’s fraudulent “revenue” in 2000 rose 151% YoY and cost many growth investors a pretty penny.

Enron’s “Revenues” 1996-2000 An investor should swarm to buy any significant dips on a stock that they are confident in as long as the underlying fundamentals and thesis of the company have not changed.

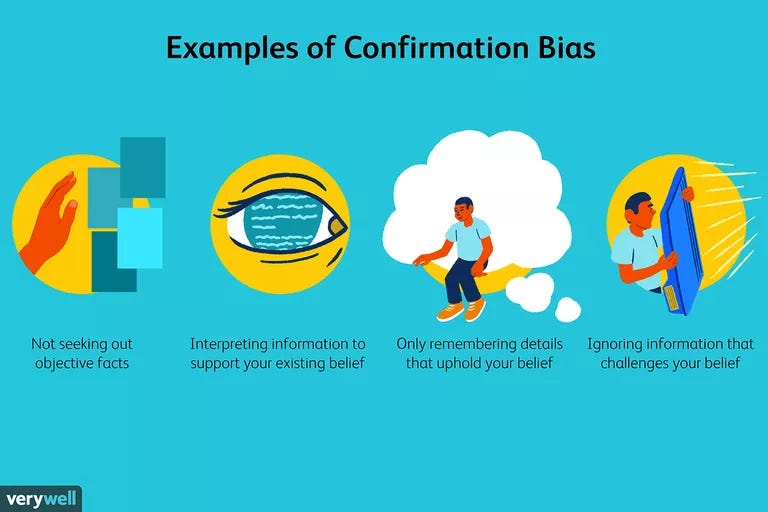

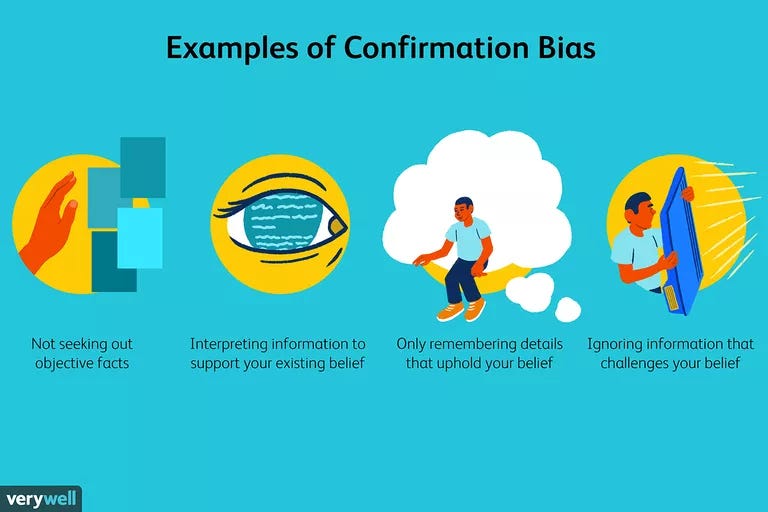

Confirmation Bias

Example: Jenny decides to invest in Company X, a penny stock, after reading several positive news article stating that upon FDA approval of their new drug, Alphaneutra, Company X could possibly double, or even triple in value. She searches for Company X on Twitter and Stocktwits and finds a vibrant community rallying behind Company X with nothing but positive things to say about the company and their future potential. Jenny excitedly makes her purchase without even glancing at the company’s financial reports due to her newfound confidence gained by reading opinions online.

2 months later, the FDA declines Alphaneutra for approval and Company X plummets 60%.

Confirmation bias is the tendency to search for and filter new information in a way that supports a preconceived notion. To avoid confirmation bias, an investor should do their own due diligence and form an investment thesis by reading a company’s annual and quarterly financial statements and any other reports or press releases. Opinion pieces are beneficial as well, but should be taken with a grain of salt. An investor should seek contrarian views in the form of playing the Devil’s Advocate or by reading articles published by reputable sources with a differing opinion.

Mainstream Fallacy

Example: The year is 2012 and Apple just aired their much anticipated iPhone 5 press conference. Jenny decides that Apple is a fantastic company and plans on buying shares. Jenny asks her friend, Jimmy, for his opinion, and his response is “Apple has been public for 38 years. Literally every person on the planet knows about it. If you’ve already heard about it on the news, it’s too late to invest.”

The Mainstream Fallacy occurs when an investor rationalizes not to buy a company solely because the company is already widely known. However, a stock’s price is based on future cash-flows, not present knowledge. Innovative companies with consistent demand will continue to innovate for longer than most people will expect, and Apple certainly fits that saying. There’s no guarantee that Apple will exist in 10 years, but there is also no reason to believe that Apple will fail anytime soon. Apple continues to bring in hundreds of billions of dollars of revenue each year, all the while expanding their loyal consumer base and massive inventory of innovative and name-brand products.

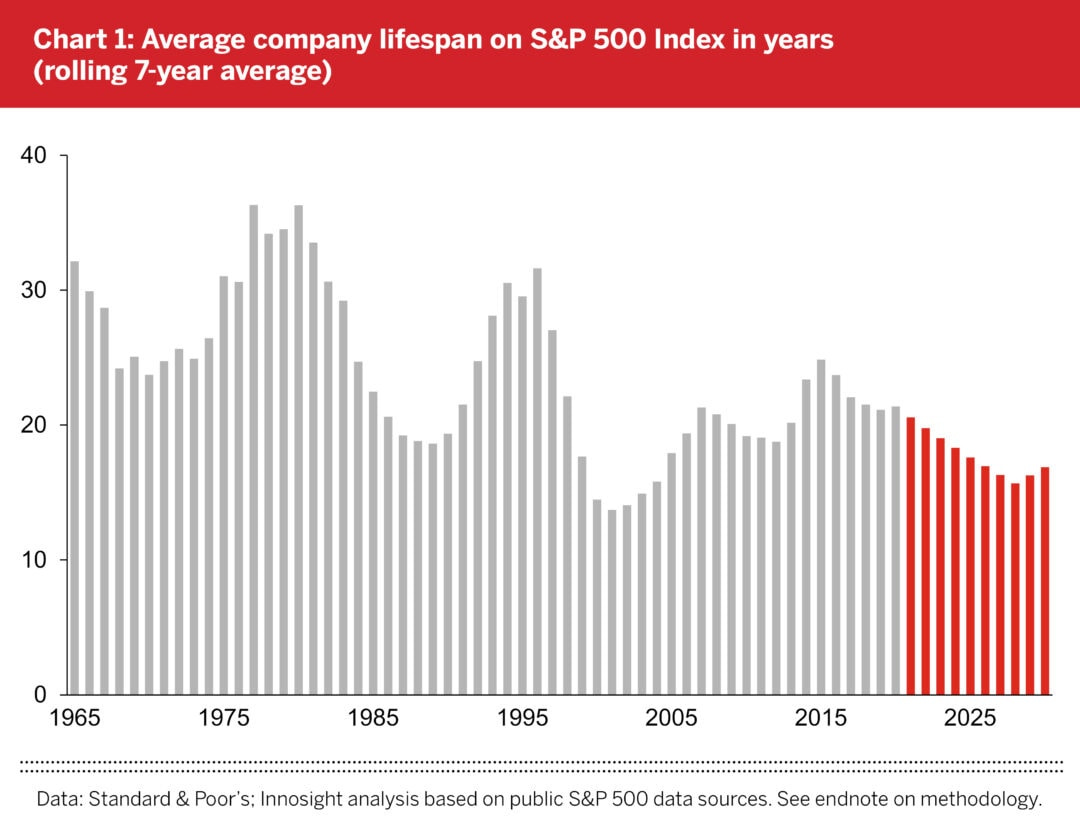

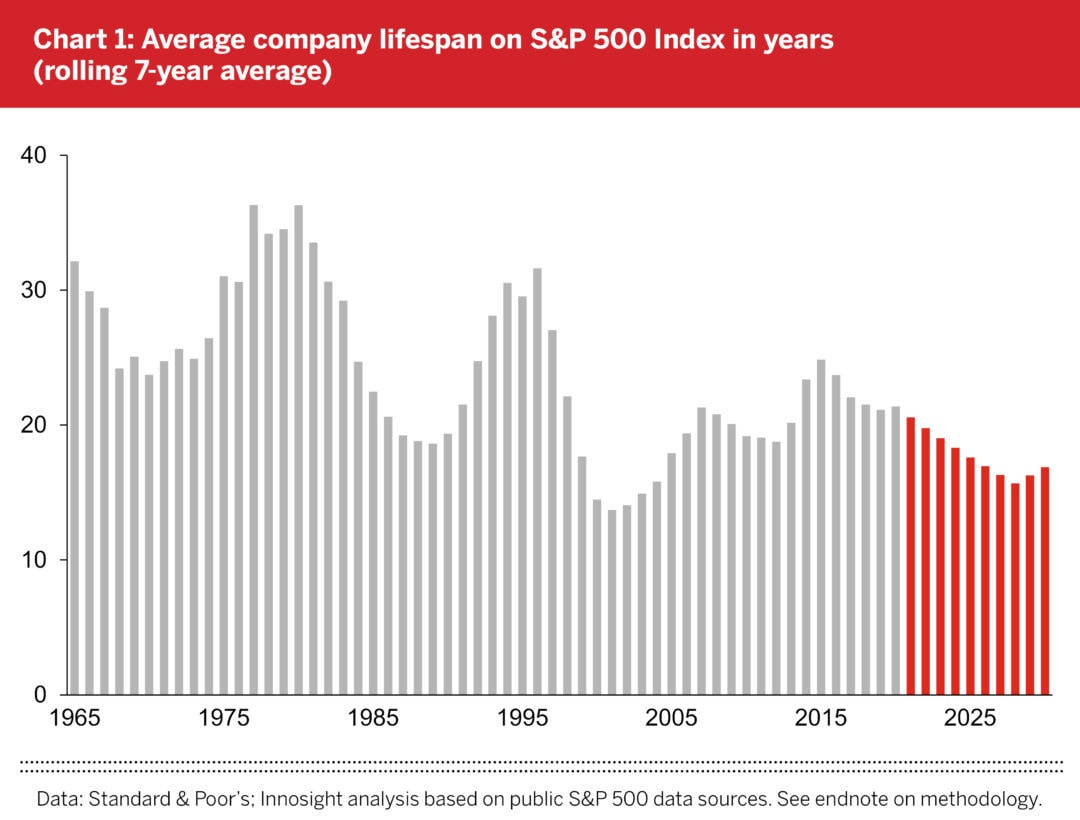

Jimmy has a point if he is basing Apple’s longevity on statistics. A study done by Innosight concluded that the average lifespan of a company listed in the S&P 500 in 2020 was 21 years. In 1973, it was 35 years. By 2027, an estimated 75% of the companies listed in the S&P 500 in 2016 may not exist due to being bought out, merging, or going bankrupt. Additionally, only 53 companies from the 1955 edition of the Fortune 500 made it on the list in 2018. However, Apple is by no means your “average” S&P 500 company.

The deadline for hedge funds and institutional investors to submit their Q2 13F form is August 16. I’m really excited to analyze the updated positions of all the top-performing hedge funds after a volatile quarter for you guys. Get ready!

For Your Eyes Only - Hedge Fund Insights

Please don’t hesitate to send me topic recommendations, suggestions, or general questions. You can contact me by email: HedgeVisions@gmail.com, or by Twitter messages @HedgeVision

Source #1 - Enron 2000 Annual Report