2021 - A Year in Review

2021 - A Year in Review

Plus, YTD Results as of Dec. 31st, 2021

What. A. Year. After all has been said and done, I’m glad 2021 is over, but also appreciative of all the connections and insights that I’ve managed to pick up. It was a challenging year in the markets, not only for retail investors, but for hedge funds as well. Many veteran fund managers, such as Tiger Global’s Chase Coleman, failed to beat the benchmark S&P 500 index. Coleman managed to squeeze out a gain of 3% as of November.

While challenging, the market provided countless lessons this year that has helped reinforce my investing strategy. As I believe, nothing financially imprints itself on you more than a moving losing event. With that said, I wanted to go more in depth on my best and worst trades this year.

Best Trades of 2021

Microsoft (MSFT)

I bought a 6% portfolio position in Microsoft during March of this year near $230. Additionally, I previously had a 1% position. After gaining experience and having friends and family in the corporate world, it was just too obvious that MSFT was a dominant player in the business industry. With that said, I do firmly believe Apple products are superior based on personal experience; however, Microsoft remains the dominant player in professional settings.

Do I believe the tide will shift one day in that Apple will dethrone Microsoft in the professional setting? I think it’s likely and would not hesitate to switch my Microsoft position for Apple if this ever occurs. Nonetheless, Microsoft remains the dominant player and returned a phenomenal 54% during 2021. Microsoft now accounts for 9.9% of my portfolio and is my second largest position.

Selling RingCentral (RNG) at $260 for Facebook (FB) at $326

I really dodged a bullet with this one. Today, RingCentral trades at $187, down 28% from my selling point. Meanwhile, Facebook trades at $336, up 3% from my purchase point. The RingCentral position represented about 3% of my portfolio at the time of sale.

I had held RNG because I believed the company would benefit from the digital transition to work from home due to the pandemic. However, the stock remained stagnant for over a year and while earnings weren’t horrible, they also weren’t extremely impressive. After conducting further analysis of EV/GP, EV/EBITDA, EV/Sales, profit margins, free cash flow, and revenue growth against competitors FIVN, ZM, CSCO, and MSFT, I concluded that competition was too strong in the space to continue my investment. To be honest, my research at the time pointed to ZM as a much superior investment. This led me to purchase a small 1.3% position in ZM, which has since declined by 45%. I continue to hold the position and have not added to it.

The creeping thought of opportunity cost was too much for me, and so I decided to purchase FB, which I had sights on for a while. This purchase was about a month before Facebook announced its rebrand to Meta Platforms and its concentration on the metaverse. I solely bought Facebook to take advantage of its powerful advertisements platform that continues to rake in billions of dollars from businesses of all sizes. I’m not exactly sure how successful Facebook’s metaverse campaign will be, and I won’t try to predict the path to innovation.

As Alex Sacerdote once said:

“Growth investors will occasionally find an attractive S-curve, but the important piece really is competitive advantage and operational abilities. In smartphones, Apple created half a trillion dollars in wealth but HTC, RIM, Nokia, Motorola, and LG destroyed value. Several went bankrupt and didn’t make a dime out of the smartphone S-curve.”

If the metaverse turns out to be the next “big thing,” I’ll do my best to follow the trend and invest in the leaders of that industry.

Honorable Mentions:

Buying Cloudflare (NET) at $70 and selling at $120 within 3-4 months for a 71% gain (2.5% position). Granted, I sold extremely early, as Cloudflare skyrocketed to as high as $220. Cloudflare remains a giant in the content delivery network (CDN) and cybersecurity world, so I may buy back shares in the near future.

Buying Unity (U) as a 1.4% position at an average price of $105. In my opinion, Unity represents a picks and shovels play for gaming design infrastructure and the metaverse. Unity now accounts for 1.9% of my portfolio.

Worst Trades of 2021

Buying Peloton (PTON) at an average price of $110 and selling for a 50% loss at $55.

I’ll admit I felt for the hype surrounding PTON amid the coronavirus pandemic and the trend to at-home digital fitness. When I did my initial research for the company, I compared the market cap of PTON to several gyms, like Planet Fitness (PLNT) and Life Time Group (LCUT). I found out that PTON’s market cap was greater than every single one of its competitors by a wide margin based on higher valuation multiples. This troubled me, but the forecasts for large user growth and revenue ultimately drove me to purchase the name at a 3.5% portfolio weight

In September/October, I failed to take into account the severity of the supply chain issues. I blindly remained confident in my pick and didn’t stop to think about the potential consequences, which turned out to be not so potential, but rather guaranteed. Peloton’s hardware is the source to customer acquisition, and with mass delays and resource acquisition bottlenecks, customer acquisition declined as well.

Peloton reported horrendous Q3 earnings and the stock tanked more than 20% shortly after. Executives in the conference call quoted the word “supply chain” numerous times. In hindsight, the earnings report shouldn’t have been a surprise, and my major error lied in being nonchalant with macroeconomic factors. This was a costly learning experience that I am grateful for.

Holding Alibaba (BABA) for a 45% loss.

It’s safe to say I underestimated the effects that restrictive regulatory policies can have on equities. BABA had a horrific year, starting off with Jack Ma criticizing the Chinese state-owned banks and regulators. A domino effect of strict regulations followed, which led to BABA tumbling almost 50% in 2021. I still remain largely bullish on the company and theme of e-commerce itself. BABA is currently a 1.7% position for me, and I have not sold any shares.

Lesson learned: Don’t underestimate the power of the government. There is a dilemma where the threat of regulatory policies may outweigh potential returns. Meanwhile, BABA trades at an extremely low multiple, especially when compared to peers.

Honorable Mentions:

Buying ZM at $340 as mentioned earlier.

Selling NVTA for a 30% loss. I bought a 3% initial position at an average cost of $44. NVTA skyrocketed to as high as $60, but I didn’t sell any of my position. Biotechs are tricky to say the least, especially when you don’t fully understand them. After a strong 2020, the majority of biotech names faltered during 2021.

An investor should be willing to admit their mistakes and take losses as a learning lesson. Fool me once, shame on you. Fool me twice, shame on me. Every year, I learn new things insights from the market that let me reflect on my mistakes and strengthen my investment strategy.

Invest in companies you understand with a history of excellence.

I lost a decent chunk of profits this year from investing in hyped-up companies that I didn’t fully understand. For example, I strayed from my investing style of not investing in certain industries. These industries are: biotech, AI, and energy. I invested in biotech via Invitae (NVTA) and AI through UiPath (PATH). NVTA was an absolute mistake, as it seems the company is content on burning through cash and staying unprofitable in the meantime. Such is the risk with biotech companies, as the industry boasts high expenses in order to succeed. Furthermore, biotech had a unsatisfying 2021. The iShares Biotechnology ETF returned 1.4% in 2021, underperforming the S&P 500’s return of 28.7%.

I remain slightly bullish on the future of PATH, but again, opportunity cost is a central theme of my investment strategy. Plus, my technical understanding of how the company’s technology operates and fares with competitors is not up to par, so I would feel much safer investing in a company that I understand. MSFT is a major competitor for PATH as well.

It’s a fact that past performance is not indicative of future performance. However, what past performance lends investors is a rep sheet of management’s actions, execution, and reputability throughout the years.

Don’t buy and hold. Buy and continually research. Hold if the thesis remains intact.

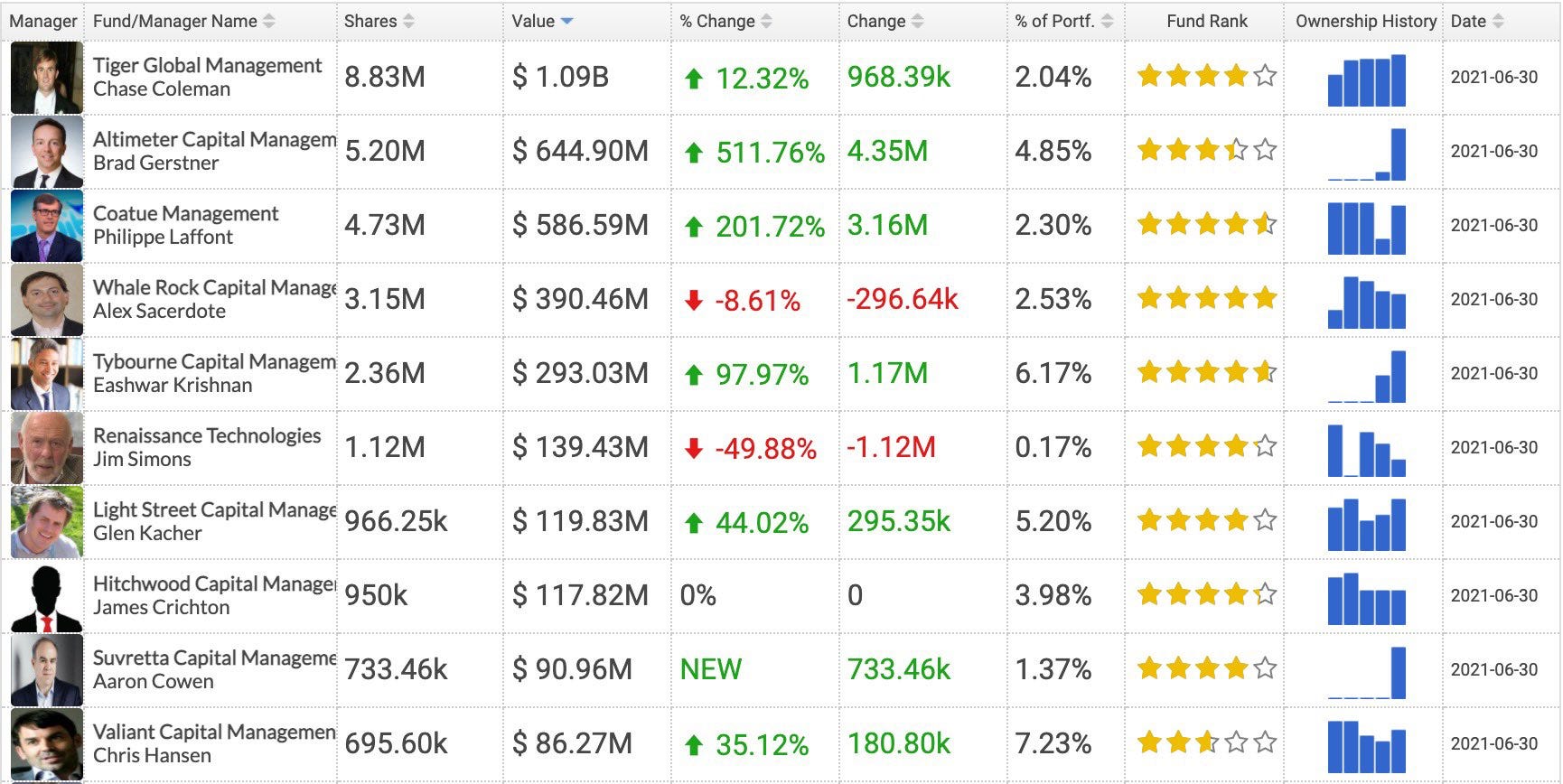

PTON taught me this the hard way this year. I had fallen for the allure of the “next big thing” in at-home fitness. Plus, several big name institutional investors had recently purchased as well when I was conducting initial research. These include: Tiger Global, Altimeter Capital, Coatue Management, Whale Rock, and Tybourne Capital. Hedge fund ownership should be included in an investment strategy, but the strategy shouldn’t solely focus around it. An investor should always personally conduct research into a stock before purchasing it. PTON in 2021 shows that even the best institutional investors can be wrong.

Here are the top hedge fund holders of PTON stock as Q2, June 30th, 2021. PTON stock closed at $124 that day.

You can see that the list tops off with several notable funds: Tiger Global, Altimeter, Coatue, Whale Rock, etc.

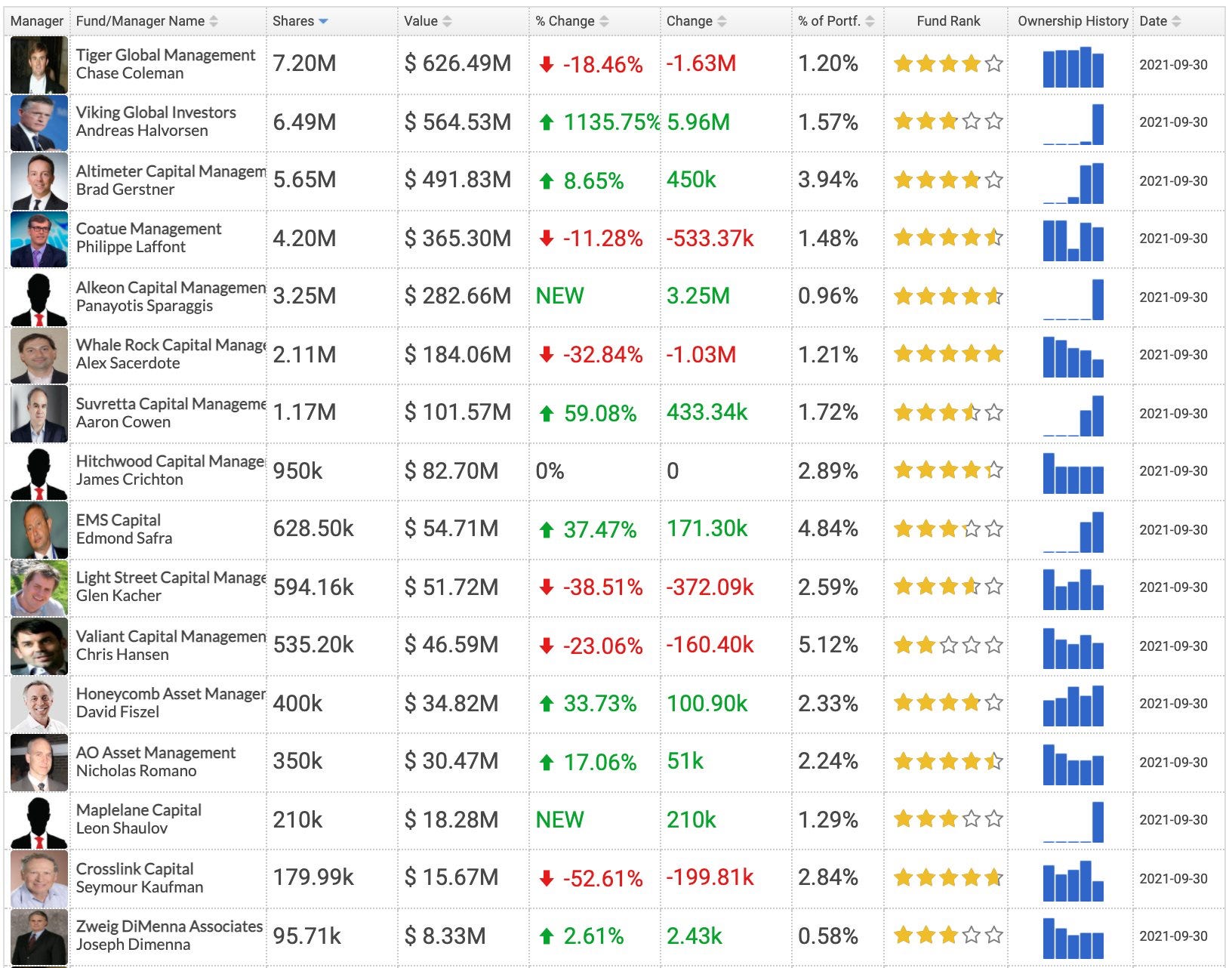

Now, compare that list with the top hedge fund holders as of Q3, September 30th. PTON closed at $87 that day.

Tiger Global, Whale Rock, and Coatue all decreased their positions during Q3. Altimeter actually increased its position during the quarter. However, CEO Brad Gerstner stated in a CNBC interview last month that he had completely exited his position. Today, PTON trades at $35.

Lesson learned: Investments must be continually evaluated, and investors should be willing to admit that they were wrong and take a loss. Even the best fund managers make mistakes, but they are quick to recognize and correct them.

Year-to-date (YTD) Performance as of Dec. 31st

December YTD & YoY Performance

Personal Return - YTD (Year to Date): 18.97%

S&P 500 Return - YTD: 28.19%

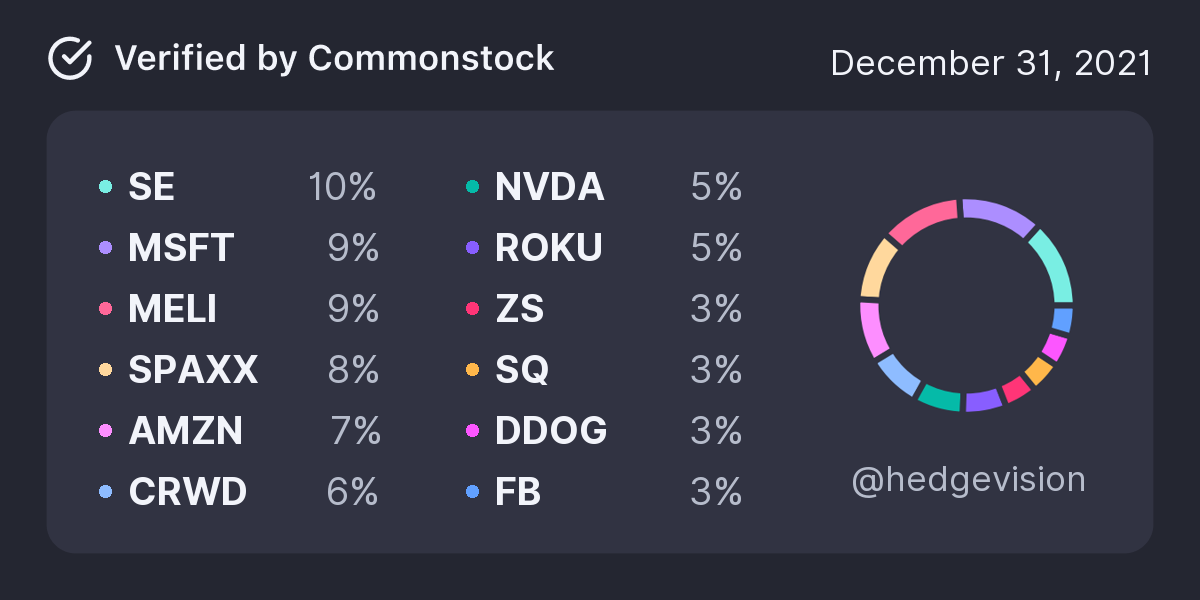

Personal Holdings

25 total positions

91.9% invested, 8.1% cash

SE: 10.3%

MSFT: 9.9%

MELI: 9.7%

AMZN: 7.2%

CRWD: 6.4%

NVDA: 5.9%

ROKU: 5.1%

ZS: 3.8%

SQ: 3.7%

DDOG: 3.7%

FB: 3.6%

CRM: 3.1%

TWLO: 3.0%

AAPL: 2.8%

PYPL: 2.6%

Rest of Portfolio: 11.1% - U, CPNG, BABA, ESTC, ADYEY, UBER, SNAP, ZM, AMD, ZI

Top 10 Holdings account for 65.7% of portfolio

Top 15 Holdings account for 80.8% of portfolio

8.1% cash position

Hedge Vision - Institutional Insights

Please don’t hesitate to send me topic recommendations, suggestions, or general questions. You can contact me by email: HedgeVisions@gmail.com, or by Twitter messages @HedgeVision